| |

By Dinesh Garg

B.Com., L.L.B. F.C.A.

GIFT as simple means, any sum or in kinds given to an Individual or HUF without any consideration or inadequate

consideration and it will not be liable to be taxed as income but the legal Perception also kept in mind :-

Where any sum of money exceeding Rs. 25,000/- is received without consideration by an Individual or HUF from

any person on or after September 2004, the whole of such sum shall be chargeable to tax as Income from Other

Sources . However, with effect from 1st April, 2006 it came to be provided vide section 56(2) (vi) that such

receipt from one or more persons aggregating to more than Rs. 50,000/- in a financial year shall be treated as

income in the hand of the recipient Individual or HUF. In the above regard, exception have been carved out in

respect of any sum of money received from any relative (as defined for purpose of this section) or on the occasion

of the Marriage of the Individual or under a will or by way of in heritance & some others.

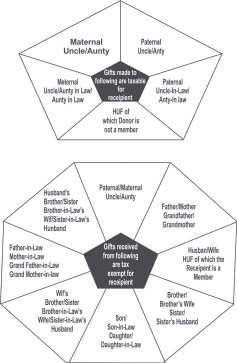

One of the important exception provided, gift received form relatives i.e. out of natural love & affection for this

purpose the relative has been defined to include the individual’s spouse, brother or sister of the individual or

spouse, brother or sister of either the Parents of the individual, any lineal ascendant or descendant of the individual

or spouse & finally the spouse of any of the above-referred persons. However, cousins, nephews & nieces have

been kept out of the list.

The finance Act, 2012 has widened the definition of relative under section 56(2) (vii) by Providing that in case of

a Hindu undivided Family, any member thereof shall be treated as a relative. Therefore, an HUF can now make or

receive gifts, to or from any of its members. However, incase of any gift being made by an individual to his HUF,

the impact of the clubbing provision under section 64(2) needs to be borne in mind.

Section 56(2) (vi) had cast Income-tax liability only in respect of a ‘gift of any sum of money exceeding Rs.50,000’.

In view of this clear language, any gift received in kind (not being any sum of money) clearly fell outside the

liability for income-tax, irrespective of the value of such gift.

However as per the new provisions of section 56(2)(vii) introduced with effect from 1" October, 2009, in case of

nine Specified Properties as mentioned hereunder, received by an Individual or HUF, either by way of gift or for

a purchase consideration that is treated by the Assessing Officer as inadequate, the market value of such gift or

the differential value of such purchase, if exceeding Rs.50,000, will be taxed as income from other sources :

i. Land and building ;

ii. Shares and securities ;

iii. Jewellery ;

iv. Archaeological collections ;

v. Drawings ;

vi. Paintings ;

vii. Sculptures ;

viii. Any work of art ;

ix. Bullion (with effect from 1st June, 2010).

Interestingly, with only nine properties specified in the hit list, a host of other valuables such as motor cars,

electronics, furniture, air tickets etc. have still been kept out of the tax purview and you can thus enjoy the luxury

of receiving gifts of any of these even beyond October, 2009.

|

|

| |

Legal Procedure of gift :- Under the Transfer of Property Act, while the gift of an immovable Property cannot be

effective or Complete till the execution of a registered gift deed, no such requirement is prescribed in regard to

a gift of a movable property. In an other cases it would, however, be advisable for you to address a forwarding

letter to donee stating clearly that you are making a gift to him/her out of natural love & affection mentioning

the detail of gifted property. In case of gift of Shares, units or bonds, it would be necessary for you to execute a

transfer form for the said Purpose. |

|